Thesis: AI is moving from a computation bottleneck to a communication bottleneck. In AI factories, networking becomes part of the compute fabric. We express that shift through COHR and LITE in lasers and optical components, and MRVL in high-speed DSP/SerDes silicon. The basket is designed to own the scarce, high-barrier enabling layers, not the entire optical-networking chain. This positioning is aligned with co-packaged optics and NVIDIA’s internal photonics efforts: CPO does not remove the need for lasers, optical components, or high-speed signal-processing silicon; it pulls them closer to the ASIC and makes their performance more critical.

Review of Latest Earnings

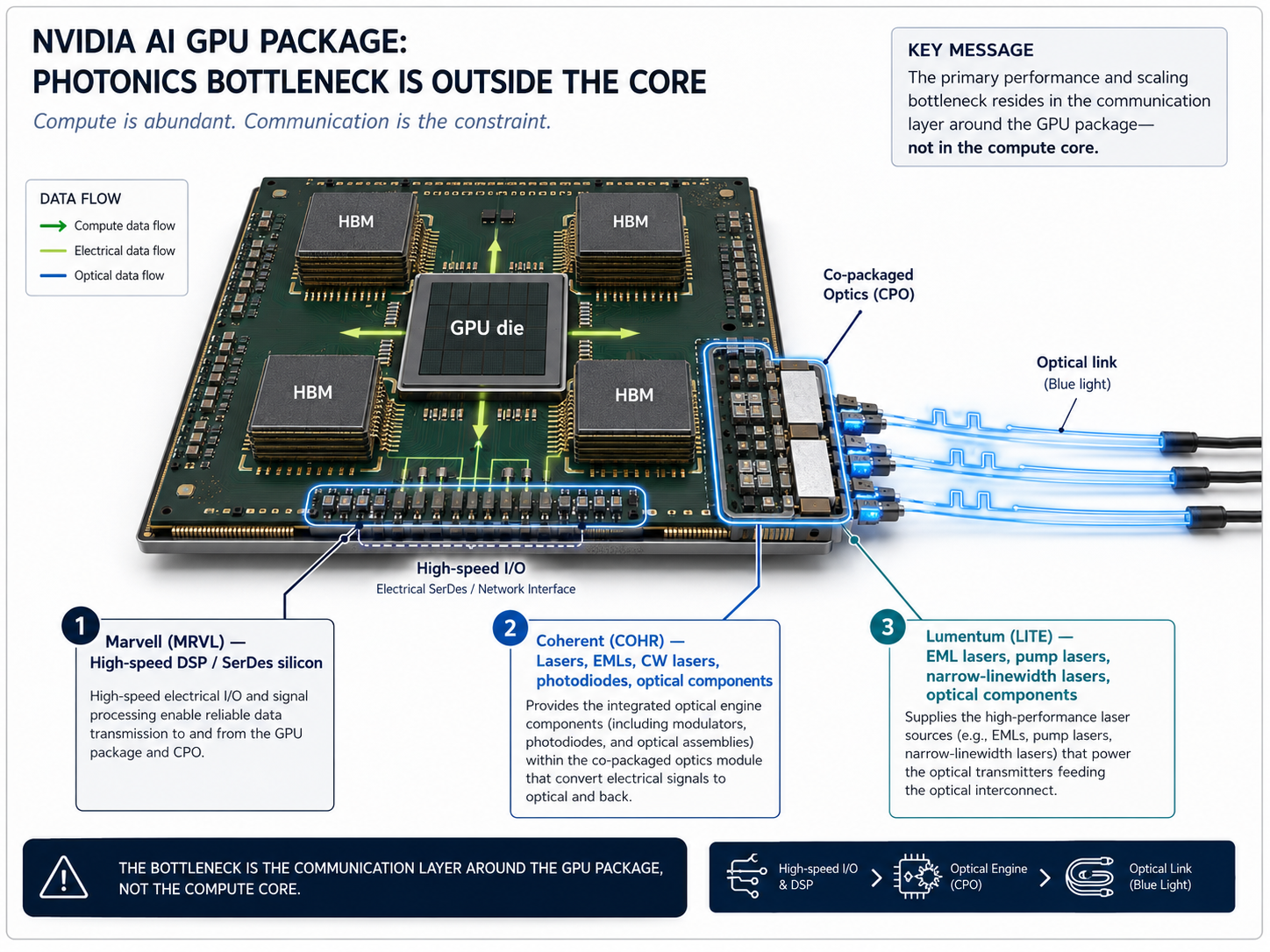

Coherent is the broad photonics platform anchor of the basket. Q3 FY26 revenue grew 27% year over year on a pro forma basis to $1.8B, with datacenter and communications now representing 75% of revenue and growing 41% year over year. The key read-through is that Coherent is scaling the physical optical supply chain required for AI datacenters: internal InP output is on track to double by year-end and more than double again by 2027, while its 6-inch platform produces EMLs, CW lasers, and photodiodes at higher yields than legacy 3-inch lines. The company is positioned across both current optical architectures and the next phase of CPO/NPO, optical circuit switching, and multi-rail transport, making COHR the broadest public-market expression of the AI photonics bottleneck.

Lumentum is the laser and CPO torque layer of the basket. Q3 FY26 revenue grew roughly 90% year over year to $808M, driven by cloud and AI demand, while non-GAAP operating margin expanded to 32.2%. The key read-through is not simply transceiver growth, but component scarcity: record 100G and 200G EML shipments, more than 120% growth in narrow-linewidth DCI lasers, 80% growth in pump lasers for scale-across and subsea applications, and continued progress in ultra-high-power lasers for CPO. LITE remains one of the cleanest public-market expressions of the laser bottleneck, though position sizing should reflect the magnitude of the stock’s rerating.

Marvell is the signal-processing layer of the photonics basket. Q1 FY27 revenue grew 28% year over year to $2.418B, with data center revenue reaching a record $1.833B. More importantly, management tied the outlook directly to AI optical networking: 800G PAM4 demand remains strong, 1.6T is ramping quickly in scale-out, TIA/driver revenue is expected to exceed a $1B annualized run-rate, and interconnect revenue is expected to grow more than 70% in FY27. MRVL is not the purest photonics exposure, but it controls one of the highest-barrier layers: the high-speed silicon required to make distributed AI communication work.

Why These Are the Bottlenecks

The earnings data confirms demand, but the investment case rests on control of the scarce layers. The highest-value layers in AI photonics are not generic fiber or standalone pluggable transceivers. They are the components that determine whether optical communication can scale with enough bandwidth, power efficiency, and reliability to support distributed AI infrastructure. In an AI factory, the bottleneck sits around the accelerator complex and network fabric, not in the compute core itself.

That points to three scarce layers: lasers, optical components, and high-speed DSP/SerDes silicon. COHR and LITE sit at the optical component and laser layer. MRVL sits at the DSP/SerDes layer. These are areas where physics, manufacturing yield, qualification cycles, and customer trust create real barriers to entry. This is why the basket is concentrated. It is not designed to own every company that benefits from optical networking; it is designed to own the layers where engineering difficulty becomes economic power.

Moat Analysis

The common feature across COHR, LITE, and MRVL is that each sits at a layer where scale alone is not enough. Capital matters, but it does not instantly create process knowledge, reliability data, customer qualification, or high-yield manufacturing capability.

Coherent has the broadest vertical exposure across the optical stack: materials, InP manufacturing, EMLs, CW lasers, photodiodes, transceivers, silicon photonics, CPO/NPO, and datacenter optical systems. Its moat is breadth plus manufacturing scale.

Lumentum has the cleanest exposure to the laser bottleneck. Its strength in EMLs, DCI lasers, pump lasers, ultra-high-power lasers, and optical circuit switching gives it direct leverage to the optical layers that become more critical as AI networks scale.

Marvell owns the high-speed signal-processing and connectivity silicon layer. DSP/SerDes silicon is one of the hardest parts of the stack to replicate because performance depends on mixed-signal design, signal integrity, power efficiency, software/firmware, and deep customer integration.

The result is a concentrated basket across three durable control points: Coherent’s optical platform breadth, Lumentum’s laser and CPO exposure, and Marvell’s high-speed signal-processing silicon.

Leave a comment